What is the name of form 5. Appendix to the balance sheet. History of the document

Today, we will consider a rather important document in the economic sphere of activity of large enterprises, namely Appendix to the balance sheet (form No. 5)– form and . the document has its own unified form No. 5, which is established by the legislation of the Russian Federation. Small businesses should not fill it out, namely those structures that are not subject to audit, as well as all non-profit public organizations. In the new application forms, some line codes are not specified, so you must assign them yourself.

Let's look at the sections of filling out form No. 5:

“Article No. 110 of the balance sheet “Intangible assets”. Tables No. 1 and 2 indicate the primary value of assets, followed by total depreciation. Table No. 1 records acquired and written-off assets throughout the year.

Balance sheet article 120 “Fixed assets” and other lines about existing values. This section consists of 2 tables. The first reflects the availability of fixed assets and their movement, which occurs at the end and beginning of the period. The second table deciphers the initial cost of fixed assets that were spent on conservation or rental, depreciation, prices of leased objects, revaluation of fixed assets, the primary value of real estate that has not yet been registered in the reporting year.

Line No. 135 deciphers “Profitable investments in tangible assets” (2 tables). The first describes investments at the end and beginning of the year, as well as their movement in a given period. The second table shows the depreciation of all deposits.

“Costs for design, research and technological work.” It serves to describe information about these expenses that are incurred for the needs of the enterprise. The first table describes all R&D costs and expenses for technological work. The second reflects information on work that has not yet reached completion and has not yielded any results.

“Costs on natural resources” reflect all costs associated with the development of deposits, carrying out all kinds of geological exploration, as well as the study of minerals and more.

Lines 140 and 250 decipher the “Financial investments” of the enterprise.

“Accounts payable and receivable” are described in lines 610,510,240 and 230.

"Costs by Cost Elements." This line describes the organization's expenses for intra-business activities.

Articles 950 and 960 “Provisions” decipher information about existing values.

“State assistance” describes the subventions, subsidies and other budget funds received by the organization that are spent on the needs of the enterprise.

In our article, you can familiarize yourself with writing an appendix to the balance sheet (form No. 5) - a form, a sample of filling, as well as which sections it includes, and what exactly they describe.

Appendix to the balance sheet (form No. 5)

The financial statements also include an Appendix to the Balance Sheet (Form No. 5). It deciphers the data from Form No. 1 “Balance Sheet”.

The balance sheet appendix consists of ten sections:

Intangible assets;

Fixed assets;

Profitable investments in material assets;

R&D expenses;

Expenses for the development of natural resources;

Financial investments;

Accounts receivable and payable;

Expenses for ordinary activities;

Provisions;

Government assistance.

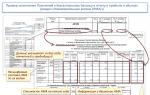

Each partition represents one or more tables. Organizations enter line codes in these tables in accordance with Order of the Ministry of Finance of Russia dated November 14, 2003 N 102n. But this Order does not contain codes for all lines of Form N 5. Therefore, the organization can determine and enter them independently. It is more convenient to do this on an accrual basis.

Section I. “Intangible assets” - here is a breakdown of the intangible assets owned by the organization.

The section consists of two tables. The first table, “Initial cost of intangible assets,” indicates data on the receipt and disposal of intangible assets. In this table you need to provide data on the initial cost of intangible assets owned by the organization.

Table 1 consists of the lines:

010 "Intellectual property objects (exclusive rights to the results of intellectual activity)";

020 "Organizational expenses";

030 "Business reputation of the organization";

040 "Other".

If an organization owns intangible assets that do not belong to any of the listed types, then data on these assets must be indicated in the “Other” line.

All rows of Table 1 are filled out in accordance with the same principle. For each type of intangible asset, the following information is indicated:

Availability at the beginning of 2004;

Admission within a year;

Disposal during the year;

Availability at the end of 2004

Table 2 “Depreciation of intangible assets” - in this table you need to provide data on the amount of depreciation that is accrued on the organization’s intangible assets. Only those organizations that account for depreciation on intangible assets in a separate account should fill out this table (use the first method of reflecting accrued depreciation in accounting).

Section II. “Fixed assets” - this section provides information about the fixed assets owned by the organization. The section consists of two tables.

The first table, “Original cost of fixed assets,” provides data on the initial cost of fixed assets.

Table 1 consists of the following rows:

Facilities;

Cars and equipment;

Vehicles, tools;

Industrial and household equipment;

Working, productive and breeding livestock;

Perennial plantings;

Other types of fixed assets;

Land plots and environmental management facilities;

Capital investments for radical improvement of land.

Table 2 “Depreciation of fixed assets” - in this table you need to indicate data on the organization’s fixed assets.

Line 140 “Depreciation of fixed assets - total” - on this line you should indicate data on the amount of depreciation that is accrued on fixed assets.

Line 145 “Fixed assets leased out - total” - on this line the accountant reflects the initial cost of fixed assets that are leased to other organizations:

To fill out this line, an organization should use data from account 01, subaccount “Fixed assets leased to other organizations”:

Line 150 “Fixed assets transferred for conservation” - on this line you need to reflect the initial cost of fixed assets that were transferred for conservation.

Line 155 “Received fixed assets for rent - total” - this line should show the cost of fixed assets that were received for rent from other organizations.

Line 160 "Real estate objects accepted for operation and in the process of state registration"

Real estate objects are accepted for accounting on the basis of an act of acceptance and transfer of fixed assets and documents that confirm their state registration.

Table 3 "For reference"

Line 170 "Result from the revaluation of fixed assets"

In this line, the accountant reflects the increase or decrease in the residual value of fixed assets as a result of their revaluation.

Line 171 “initial (replacement) cost” - on this line the accountant reflects the decrease or increase in the initial cost of fixed assets that occurred as a result of their revaluation.

If the organization has overvalued fixed assets, then, when filling out the line “Initial (replacement) cost”, the accountant looks at the revaluation records on the debit of account 01. If a markdown of fixed assets was carried out, then to fill out this line, entries on the credit of account 01 are required. The amount of the markdown should be reflected by this line in parentheses.

Line 172 “depreciation” - on this line you need to show the decrease or increase in depreciation of fixed assets that occurred as a result of their revaluation.

Line 180 “Change in the value of fixed assets as a result of completion, additional equipment, reconstruction, partial liquidation” - gives the user of the financial statements an idea of how the initial value of fixed assets has changed as a result of their completion, additional equipment, reconstruction or partial liquidation.

If the organization did not carry out the specified activities, then dashes are placed on this line.

In section III. “Profitable investments in tangible assets” you need to provide data on profitable investments in tangible assets owned by the organization. The section consists of two tables.

Table 1 "Initial cost" is devoted to the initial cost of profitable investments in material assets. In this table you need to provide data on the initial cost of profitable investments in material assets. Table 2 reflects depreciation on profitable investments in tangible assets.

Table 2 "Depreciation" consists of only one line. It reflects data on the amount of depreciation that is accrued on profitable investments in tangible assets.

Section IV. “R&D expenses” - in this section of the Appendix to the balance sheet (Form No. 5) you need to reflect data on the organization’s expenses for R&D.

The section "R&D expenses" consists of two tables. The first reflects the actual costs of research, development and technological work. The second table is called "For reference".

Table 1 “R&D expenses” - in this table the accountant enters the amount of R&D expenses that have already been completed, but have not been formalized in accordance with the established procedure, that is, they have not become intangible assets.

Table 2 "For reference" - consists of two lines:

Amount of expenses for unfinished R&D;

The amount of R&D expenses that did not produce positive results and were charged to non-operating expenses.

In this section V. “Expenses for the development of natural resources”, the Appendix to the balance sheet reflects data on the organization’s expenses for the development of natural resources: geological study of subsoil, mineral exploration, and preparatory work.

The section "Expenditures on the development of natural resources" consists of two tables. Table 1 reflects the actual expenses, table 2 is for reference.

In Table 1, “Expenses for the development of natural resources with a breakdown,” the accountant shows the total amount of the organization’s expenses for the development of natural resources, and also provides a breakdown of these costs by type. All expenses of an organization for the development of natural resources can be divided into three groups.

The first group includes expenses for searching and evaluating mineral deposits, for mineral exploration and hydrogeological surveys, for acquiring the necessary geological and other information from third parties.

The second group includes expenses for preparing the territory for mining, construction and other work. This group includes, for example, expenses:

For the construction of temporary access roads and roads for the removal of mined rocks, minerals and waste;

To prepare sites for the construction of relevant structures, storage of fertile soil, extracted rocks, minerals and waste.

And the third group represents the costs of compensation for complex damage caused to natural resources during the construction and operation of facilities.

Table 2 "For reference" - has two lines:

The amount of expenses for subsoil areas that have not completed the search and evaluation of deposits, exploration or hydrogeological surveys and other similar work;

The amount of expenses for the development of natural resources included in the reporting period as non-operating expenses as fruitless.

Section VI. “Financial investments” - this section of the Appendix to the balance sheet provides information on the organization’s financial investments:

In columns 3 and 5 - at the beginning of the reporting period;

In columns 4 and 6 - at the end of the reporting period.

Moreover, it is necessary to separately indicate data on long-term financial investments (columns 3 and 4) and separately on short-term financial investments (columns 5 and 6). To fill out this section, you need to use account balances as of January 1 and December 31, 2004. The “Financial Investments” section consists of one table, which can be divided into three parts.

In the first part of the table “Cost of financial investments” you need to provide data on all financial investments: both those by which the current market value is determined and those by which it cannot be determined.

In the second part of the table “Current market value of financial investments”, it is necessary to separately provide data on those financial investments by which the current market value is determined.

The third part of the table “For reference” indicates data on changes in the initial cost of financial investments in the reporting period.

Section VII. “Receivables and payables” - in this section you need to provide data on the amount of receivables and payables:

The table in this section is divided into two parts:

1) Accounts receivable is the amount of money that an organization must receive from other organizations and individuals.

2) Accounts payable is the amount of money that an organization must pay to other organizations and individuals. To fill out this part of the table, you need to use the balances of the credit accounts and subaccounts for accounting for settlements.

Section VIII. “Expenses for ordinary activities” - is intended to show the enterprise’s expenses for its main activity. Moreover, costs are given by cost elements. Column 3 indicates the amount of expenses incurred in 2004, and column 4 indicates expenses that occurred in 2003.

In Section IX. “Provides” The appendices to the balance sheet should indicate the amount of security issued and received by the organization:

The table can be divided into two parts:

1) “Provisions received” - this part of the table reflects the amount of security received.

In the line “Received - total” you need to show the amounts of all received collateral. And in the line “Bills” you need to indicate the amount of bills that were received by the organization to ensure the fulfillment of obligations. To fill out this line, you need to use the debit balance of account 62 “Settlements with buyers and customers”, subaccount “Bills received”.

The line “Property pledged” reflects the value of the property that is held by the organization as collateral. Below is a breakdown of property pledged by type:

Fixed assets;

Securities and other financial investments;

To fill out this line, you need to use analytical data on the debit of off-balance sheet account 008 “Collateral for obligations and payments received.”

The fulfillment of contractual obligations can be ensured, in addition to the pledge, by the retention of the debtor’s property; surety; bank guarantee; deposit; in other ways provided for in the agreements.

If the organization received these types of collateral, then to reflect them you need to enter additional rows in this part of the table. And to fill in additional lines, you must also use the debit balances of off-balance sheet account 008.

2) “Provides issued” - in this part of the table, the accountant shows the amount of security that the organization issued.

The line “Received - total” indicates the amount of all issued collateral. In the line “Bills” you should indicate the amount of bills issued by the organization to ensure the fulfillment of obligations. To fill out this line, you need to use the debit balance of account 60 “Settlements with suppliers and contractors”, subaccount “Bills issued”.

The line “Property pledged” reflects the value of the property that is held by the organization as collateral. Below is a breakdown of the property pledged by type: fixed assets; securities and other financial investments; other.

To fill out this line, you need to use analytical data on the debit of off-balance sheet account 009 “Securities for obligations and payments issued.”

Section X. “State assistance” - this section is devoted to state assistance, which means an increase in the economic benefit of the organization as a result of the receipt of assets (cash, other property).

Subsidies and subventions are budgetary funds and are provided to organizations on a free and non-refundable basis for the implementation of targeted expenses.

The assets and liabilities of the enterprise shown in the balance sheet.

What is Form 5 of financial statements

This appendix provides more detailed and detailed information on individual sections of the balance sheet, including reflecting the reasons and methods of occurrence of the amounts in the accounting report, justifying its sections and paragraphs (Order of the Ministry of Finance No. 66n dated July 2, 2010). Appendix 5 to the balance sheet is required to be provided by all enterprises engaged in entrepreneurial activities, except for those using. only if necessary, when additional information is required on sections of the balance sheet.

Form 5 involves filling out tables for various groups of enterprise assets according to their financial affiliation. When filling out some lines of the application, you must use codes approved by the joint order of the Ministry of Finance of the Russian Federation No. 102n and the State Statistics Committee of the Russian Federation No. 475 dated November 14, 2003. For the remaining lines, the codes are approved by the enterprises themselves.

Filling procedure

Structure

Form 5 consists of several sections, which have their own characteristics when filling out. The number of completed tabular blocks in the Form 5 appendix must correspond to the amount of information on the lines of the balance sheet. When drawing up a balance sheet, it contains references to specific ones.

Intangible assets

The form was approved by order of the Ministry of Finance of the Russian Federation No. 67n dated July 22, 2003. But the enterprise has the right to develop such a form itself, taking into account the basic requirements for it according to PBU 4/99. You can do it with us for free.

The basis for entering information is all primary accounting documents of the enterprise. In addition to detailing the various balance sheet items, Form 5 gives a more complete and understandable picture of the organization’s financial position.

Is it possible to do without form 5

Appendix Form 5 is a clarifying document, the need for which has been confirmed by practice: some time ago it was replaced by an explanatory note, which led to confusion, since the format of the explanatory note did not fit into the general format of the financial statements. Therefore, this application was reintroduced and became a necessary component. That is, the inextricable connection between balance and applications to it has been proven by practice.

Paper forms of accounting statements, fraud on the Internet, the use of UTII - you will find all this in the video below:

Why do you need Appendix 5 to the balance sheet and who should draw it up?

The main objective of accounting reporting is to provide complete and reliable information about the company's activities to all interested users. The balance sheet form itself cannot always provide all the necessary data, since the indicators in it are presented in an aggregated form.

Consider, for example, the article “Fixed assets”. In the balance sheet this is one figure, but in fact it can hide dozens, hundreds and even thousands of different objects. The same applies to debt indicators, financial investments and some other balance sheet items. Form 5 (Appendix No. 3 to the balance sheet) is used to detail them.

All legal entities must fill it out, except for those who are granted the right to conduct simplified accounting by the Law “On Accounting” dated December 6, 2011 No. 402-FZ. We are talking about the following organizations:

- Participants of the Skolkovo project.

The list of these persons was approved by clause 4 of Art. 6 of the above law.

What does Form 5 for the balance sheet consist of?

Form 5 includes several sections, each of which deciphers a specific reporting indicator. If the balance sheet contains data on a particular item, fill out the corresponding table in Form 5.

The complete list of articles to be deciphered using Form 5 is as follows:

- Intangible assets and R&D expenses.

- Fixed assets and capital investments.

- Financial investments.

- Inventories.

- Accounts receivable and accounts payable.

- Production costs.

- Estimated liabilities.

- Government assistance.

As already mentioned, an organization may not fill out this form if it maintains simplified accounting. But we should not forget that simplified accounting does not cancel the general reporting requirements, in particular, completeness and reliability.

Appendix to the balance sheet form 5 - form and filling procedure

The currently valid form 5 was approved by order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n. From 06/01/2019, the form as amended, approved, is used. by order of the Ministry of Finance dated April 19, 2019 No. 61n.

The changes in the updated form are minor:

- The unit of measurement “million rubles” has been excluded. and its code is “385”. Now all data is entered in thousands of rubles.

- The code "0710005" has been removed.

Don't know your rights?

Most of the tables included in it are turnover sheets. They contain information about the corresponding asset (liability) at the beginning of the period, its change during the period and indicators as of the last reporting date.

The difference can only be in the degree of detail of the data. For example, fixed assets and accounts receivable often include a very significant number of objects or counterparties. Therefore, information on these items is usually shown by group. And the number of intangible assets, as a rule, is smaller, therefore, they can be detailed by type.

In addition, the report includes a number of tables in a different format that provide additional information on individual balance sheet items:

- For intangible assets, information is allocated on objects created by the organization itself, and intangible assets with a fully repaid value.

- The following information is provided for fixed assets:

- changes in the value of objects as a result of additional equipment, reconstruction or partial liquidation;

- other use of fixed assets (letting and receiving, pledging, conservation, etc.).

- For financial investments, information about their other use (for example, collateral) is shown separately.

- Inventories also provide information about the property pledged as collateral.

- For receivables and payables, information about overdue debts is highlighted.

- For estimated liabilities, information about their collateral is shown separately.

All “turnover” indicators are given for the reporting and previous year. All information relating to a specific date (for example, balances of overdue debts) is indicated as of the reporting date and the last dates of the two years preceding the reporting period.

How is the supplement to the 2019 balance sheet - Form 5 related to other reporting forms?

This application mainly deciphers balance indicators. In the balance sheet form there is a column “Explanations”, which indicates the numbers of tables in Form 5, which decipher the corresponding item.

In addition, Form 5 also contains detailed information on the financial results statement in terms of production costs for the reporting and previous year. The following main articles are highlighted:

- materials;

- salary with accruals;

- depreciation;

- others.

The same table provides information on changes in balances of finished products and work in progress.

However, Form 5 does not provide a breakdown of all balance sheet indicators. To get complete information, you need to use other applications. For example, for the item “Cash” - information from the cash flow statement, and for authorized capital - the statement of changes in capital.

In the “Explanations” balance column opposite these items, instead of the table numbers from Form 5, the names of other reports containing their details will be indicated.

Appendix to the balance sheet - Form 5 contains a breakdown of a number of indicators. All legal entities must fill it out, with the exception of those who maintain simplified accounting. As of June 1, 2019, updated Form 5 is in effect (Appendix No. 3 to the balance sheet). Explanations of indicators in Form 5 are turnover statements with details by groups or types of assets and liabilities. To obtain complete information, along with Form 5, you need to use other balance sheet applications.

Order of the Ministry of Finance No. 66n dated July 2, 2010 provides accounting reporting forms. To justify the sections of the balance sheet, Form 5 is used. It is of a clarifying nature and is intended to detail the key indicators in the balance sheet. Thanks to the presence of Form 5, it becomes possible to make an in-depth analysis of the financial situation of the organization.

Form 5 of financial statements: general information

Form 5 involves filling out the tabular elements of the balance sheet appendix for groups of assets that are classified according to the criterion of financial affiliation. The connection between the contents of the balance sheet and Form 5 is direct - the balance sheet acts as the main document, and the appendix to it performs the function of detailed transcripts of generalized indicators.

The peculiarity of filling out the tables in the appendix to the balance sheet by structures using a simplified accounting system is that they reflect the most significant indicators in Form 5. The main factor of significance for such a group of organizations is the possibility or impossibility of assessing the general financial condition. However, they do not have to fill out this form.

The amount of detailed information on the balance sheet in the tabular blocks of the application should correlate with the amount of information contained in the lines of the completed balance sheet. When creating a balance, links to explanatory documents for a specific position are provided. Form 5 does not provide an exhaustive list of indicators. Therefore, for example, when reflecting cash values in the balance sheet, a link to the cash flow statement is created in the explanation column, since Form 5 does not detail this position.

Form 5 (attachment to the balance sheet): example of completion

The nuances of filling out Form 5 can be seen using an example. The company Globus LLC has the following completed balance sheet lines:

- cost indicators for fixed assets minus depreciation, consisting of production and office equipment, the cost of which changed during the year);

- the amount of reserves (in the presented value of the indicator there are no assets pledged);

- the volume of accounts receivable, which is represented only by short-term loans, the company did not create a reserve for doubtful debts;

- available financial investments;

- monetary resources;

- authorized capital;

- the value of the organization's retained earnings indicator;

- the total amount of outstanding accounts payable formed under agreements with counterparties; there are no long-term liabilities in the total amount.

The appendix to the balance sheet will disclose details on those lines that contain links to the corresponding tabular parts of Form 5:

To detail the values of amounts for fixed assets, section 2 of the application is used, consisting of 4 blocks. The fact that the balance sheet contains a reference only to Table 2.1 indicates that during the reporting period the enterprise did not have cases of additional equipment, liquidation, or completion of fixed assets, and there are no assets in the form of unfinished capital construction.

Appendix Table 3.1 details the indicator of financial investments. The amount is reflected at historical cost, taking into account all types of receipts, accrued interest and disposals. Long-term assets are shown separately from short-term ones.

Block 4.1 contains information about the available volume of inventories and their reserve; all unpaid groups of inventories, including collateral items, are entered in table 4.2.

Section 5 is devoted to the enterprise’s debts – accounts payable and accounts receivable. The latter indicator should take into account the reserve for doubtful debts created in the institution.