Financial statements. Accounting statements: the possibility of correction (replacement) after presentation to users until the moment of approval When the balance is approved

The annual financial statements are approved at the general meeting of shareholders (participants, founders) in the manner established by the constituent documents of the organization (clause 2 of article 15 of the Accounting Law). According to Art. 47 of Law N 208-FZ issues of approval of annual reports, annual financial statements, incl. profit and loss statements and distribution of profits are decided at the annual general meeting of shareholders. This meeting is held between March 1st and June 30th.

The reliability of the data contained in the company's annual financial statements must be confirmed by its audit commission (auditor) (Article 88 of Law No. 208-FZ).

The annual report of a joint stock company submitted for approval to the general meeting must contain a note indicating its preliminary approval by the board of directors (supervisory board). If the company does not have a board of directors (supervisory board), the report is first approved by the person holding the position (performing the functions) of the sole executive body of the company. This requirement is contained in clause 3.7 of the Regulations, approved by Resolution of the Federal Securities Commission of Russia dated May 31, 2002 N 17/ps.

Preliminary approval of the report is made no later than 30 days before the date of the annual general meeting of shareholders.

According to Art. 34 of Law N 14-FZ, the period for holding the next meeting of the company at which the annual reports are approved must be determined by its charter. This meeting is held between March 1st and April 30th. Before submitting annual reports to the general meeting, they must be approved by the audit commission of the company. An audit commission is formed without fail in companies with more than 15 participants. In other cases, the formation of an audit commission (or election of an auditor) is regulated by the company's charter. If the company has an audit commission (auditor), the general meeting of participants does not have the right to approve annual reports and balance sheets in the absence of conclusions of the audit commission (Article 47 of Law No. 14-FZ).

11.4.1. Holding a general meeting of a joint stock company

One of the responsibilities of a joint stock company (JSC) is to hold an annual general meeting of shareholders, at which the most important issues are considered: the results of the year’s activities are summed up, annual reports are approved, governing and control and audit bodies are elected, and dividends are declared. Regardless of the type of company (open or closed) and the number of shareholders, the annual general meeting must be held in each joint stock company.

In a company where all voting shares belong to one shareholder, decisions on issues within the competence of the general meeting are made by such shareholder individually. However, the said shareholder also needs to, within the time limits established for the annual general meeting, make decisions that constitute its agenda.

Preparation and holding of the annual general meeting is the main organizational task of each company in the period from the beginning of the year to July.

The procedure for convening and holding the annual general meeting is regulated by Law No. 208-FZ. Errors made during the preparation and conduct of the meeting may give rise to claims against the company from shareholders who are not satisfied with the results of the general meeting.

According to paragraph 1 of Art. 47 of Law N 208-FZ at the annual general meeting of shareholders the following issues must be considered and decisions made:

Election of the board of directors (supervisory board);

Election of the audit commission (auditor);

Auditor approval;

Approval of annual reports, annual financial statements, incl. profit and loss statements (profit and loss accounts) of the company;

Distribution of profits and losses of the company based on the results of the financial year, as well as payment (declaration) of dividends.

At the annual general meeting of shareholders, other issues within the competence of the general meeting may also be resolved. Thus, its agenda must include at a minimum all of the above, as well as other issues included in the agenda by persons entitled to do so.

The decision to hold an annual general meeting is made by the board of directors (supervisory board). In companies where a board of directors (supervisory board) has not been created (this is permissible in a joint-stock company with less than 50 shareholders), the decision to hold an annual general meeting of shareholders is made by the person or body who, in accordance with the charter of this joint-stock company, is entrusted with such responsibilities. The procedure for preparing for the annual general meeting of shareholders is set out in Art. 54 of Law No. 208-FZ.

No later than 15 days after the closing of the general meeting of shareholders, its minutes are drawn up in two copies, which are signed by the chairman and secretary of the general meeting.

The requirements for the content of the protocol are established by Art. 63 of Law No. 208-FZ. It must indicate:

Place and time of the meeting;

Chairman (presidium) and secretary of the meeting;

Agenda;

Main provisions of speeches;

Decisions made by the meeting.

Minutes of general meetings of shareholders must be kept at the location of the executive body of the company. At the same time, the joint-stock company is obliged to provide any shareholder with access to them.

Annual financial statements are a source of reliable information about the financial condition and results of the company’s economic activities for the past year. Therefore, legislation and, to a greater extent, internal rules of financial institutions pay special attention to the procedure for its preparation, content and approval. Based on the indicators of the annual financial statements, the investment attractiveness of the company for potential investors and owners of its securities is assessed.

In accordance with accounting legislation, annual financial statements subject to mandatory approval the highest governing body of the company. The general meeting of shareholders (participants) of the company makes a decision on its approval.

Limited liability companies approve annual financial statements at the next general meeting of participants no earlier than 4 months and no later than 4 months after the end of the financial year. Joint-stock companies - no earlier than 2 months and no later than 6 months after the end of the financial year.

The structure of the annual financial statements includes a balance sheet, a profit and loss statement, appendices thereto, an auditor's report confirming the reliability of the statements (if they are subject to mandatory audit), and an explanatory note.

According to the Accounting Law, before drawing up annual financial statements, the company is obliged to conduct an inventory of property and liabilities, during which their presence, condition and valuation will be checked and documented.

Then, the annual financial statements must be signed by the head and chief accountant of the organization to confirm the accuracy and completeness of the information contained therein.

Annual financial statements subject to mandatory verification audit commission (auditor) of the company. Confirmation of the accuracy of the reporting by the audit commission (auditor) of the company is a necessary condition before submitting the reporting for approval by the general meeting of shareholders (participants): in accordance with clause 3 of Art. 47 of the Federal Law on Limited Liability Companies, the general meeting of participants does not have the right to approve the annual balance sheets of the company in the absence of a conclusion from the audit commission (auditor) of the company.

When preparing for the general meeting to approve the annual financial statements, shareholders (participants) must be provided with access to the annual financial statements, including the auditor’s report and the conclusion of the audit commission (auditor) of the company based on the results of the audit of the annual financial statements.

For joint stock companies that have carried out (carrying out) a public placement of bonds or other securities, the legislation specifically regulates the stages of approval of annual financial statements: 1) signing by the manager and chief accountant, 2) confirmation by the audit commission (auditor), and then 3) approval by the general meeting shareholders.

The company's annual financial statements are information open to all interested parties (banks, investors, creditors, buyers, suppliers, etc.), and are available for review and copying. The company must provide interested users with the opportunity to familiarize themselves with the financial statements.

Limited liability companies are free from the obligation to publish financial statements, except in cases provided for by law. Thus, in the case of a public offering of bonds and other equity securities, a limited liability company is obliged to publish annual balance sheets annually.

For joint stock companies, the legislation establishes more stringent rules for the disclosure of financial information.

Open joint stock companies are required to publish annual financial statements. In accordance with paragraph. 1 tbsp. 16 of the Accounting Law, publication is carried out no later than July 1 of the year following the reporting year. Closed joint stock companies are also required to disclose annual financial statements in the event of a public offering of bonds or other securities.

An open joint-stock company can publish annual financial statements only after checking and confirming them by an independent auditor (audit firm) and subsequent approval by the general meeting of shareholders. Before approving the statements, an auditor who is not connected by property interests with the company or its shareholders must be engaged to check and confirm them.

The legislation on the securities market regulates in sufficient detail the issue of disclosure and presentation of financial information by issuers. Accounting, including annual, reporting plays a key role in the disclosed documents.

According to paragraph 12 of Art. 30 of the Federal Law “On the Securities Market”, the annual consolidated accounting (consolidated financial) statements of the issuer for the last completed financial year are disclosed/provided no later than 3 days after the date of the auditor’s report, but no later than 120 days after the end of the financial year, as well as included in the quarterly report for the second quarter of the following financial year.

A joint stock company that is not subject to information disclosure requirements is obliged to publish the text of its annual financial statements on its website on the Internet no later than 45 days from the date of expiration of the deadline for submitting annual financial statements. And no later than 2 days from the date of drawing up the minutes of the next general meeting of shareholders, at which the issue of approving the annual financial statements was considered, publish on the Internet page a message about the approval (non-approval) of the annual financial statements of the joint-stock company.

The issuer is obliged to place a copy of the annual financial statements at the address specified in the Unified State Register of Legal Entities, and before the end of the term for the placement of securities - also in the places indicated in the issuer's advertising messages containing information about the placement of securities. The issuer is also obliged to provide a copy of the annual financial statements, certified by an authorized person, to the owners of securities and other interested parties upon their request within no more than 7 days.

It must be borne in mind that the disclosure of annual financial statements in accordance with the requirements of the legislation on the securities market does not relieve issuers from the obligation to publish annual financial statements in accordance with the legislation on accounting.

In addition, issuers of Russian depositary receipts are also required to disclose annual financial statements and consolidated financial statements (if any) prepared in accordance with IFRS or US GAAP in an appendix to the quarterly report. In this case, the statements must be checked by an auditor, and the auditor’s opinion must be attached to the disclosed financial statements.

Providing reports to government agencies

Annual financial statements must be submitted not only to the founders, shareholders, participants or owners of the company, but also to the territorial bodies of state statistics at the place of its registration within 90 days after the end of the year. At the same time, the annual financial statements of the organization presented must be approved the supreme management body of the company in the manner established by the constituent documents.

The date of approval of the annual financial statements is indicated directly on the first page of the balance sheet.

Placement of securities

When increasing the authorized capital by placing an additional issue of shares, a copy of the company’s financial statements for the last completed financial year and for the last quarter is provided for state registration of the additional issue of shares (not accompanied by registration of a securities prospectus).

Regarding the issue of securities with registration of a prospectus, it includes annual the issuer's financial statements for the last 3 completed financial years preceding the date of approval of the prospectus, accompanied by the auditor's report. If the issuer has been operating for less than 3 years, then annual financial statements for each completed financial year are submitted, accompanied by an auditor's report.

If the issuer has annual financial statements prepared in accordance with IFRS or US GAAP, then such financial statements of the issuer for the last 3 completed financial years preceding the date of approval of the securities prospectus, in Russian, are also attached to the prospectus.

The securities prospectus is signed by the director, chief accountant and auditor, and approved by the board of directors (supervisory board) of the company.

IPO, listing

Providing approved annual financial statements is one of the conditions for admission of securities of corporate issuers(stocks, bonds) to trading on stock exchanges in the process of placement with the passage of the listing procedure.

Thus, to the application for admission of securities to trading in the process of placement/circulation with the listing procedure on the MICEX Stock Exchange, it is necessary to attach annual financial statements in accordance with Russian accounting standards (RAS) for the last 3 completed financial years and annual financial statements in accordance with IFRS and/or US GAAP in Russian with an appendix of the auditor's report in relation to these statements.

According to the Rules for the admission of securities to trading of OJSC RTS Stock Exchange, in order to include shares and corporate bonds in the quotation list, among other things, the issuer must submit annual financial (accounting) statements in accordance with IFRS and/or US GAAP, in respect of which the audit, and accept the obligation to maintain these reports and disclose them together with the auditor’s report in Russian.

Issue of bonds

The presence of duly approved annual financial statements for 2 completed financial years is also a condition for issuing bonds in the absence of collateral provided by third parties.

The same condition must be observed when issuing exchange-traded bonds without state registration of their issue (additional issue), registration of the bond prospectus and state registration of the report on the results of their issue (additional issue). Moreover, exchange-traded bonds are admitted to trading on the stock exchange without going through the listing procedure, subject to the availability of duly approved annual financial statements for 2 completed financial years.

Increase and decrease of authorized capital

A decision to increase the authorized capital of a limited liability company at the expense of its property can be made only on the basis of data from the company’s financial statements for the year preceding the year during which such a decision was made. Attention is also drawn to the obligatory consideration of this requirement in subsection. “a” clause 9 of the Resolution of the Plenum of the Armed Forces of the Russian Federation and the Plenum of the Supreme Arbitration Court of the Russian Federation of December 9, 1999 No. 90/14.

Data from the company's annual financial statements (it is assumed that they have been approved) are necessary to determine the possibility of increasing the company's authorized capital at the expense of the company's property, including to determine whether the requirement of clause 2 of Art. 18 of the Federal Law on Limited Liability Companies, which states that the amount by which the authorized capital of a company is increased at the expense of its property should not exceed the difference between the value of the company’s net assets and the amount of the authorized capital and reserve fund of the company.

Based on the indicators of the annual financial statements, the company makes a decision to reduce the authorized capital or may even make a decision to liquidate the company.

Reorganization

When preparing for reorganization, all companies participating in it need to assess the financial condition and prospects of the companies with which they will have to combine business, or the possible consequences for the company when dividing the business.

Therefore, all persons entitled to participate in the general meeting, the agenda of which includes the issue of reorganization, are provided with annual reports and annual financial statements of all companies participating in the reorganization for 3 completed financial years preceding the date of the general meeting, or for each completed financial one year from the date of formation of the organization, if the organization has been operating for less than 3 years.

At the same time, a legal entity created as a result of reorganization (with the exception of the merging, spin-off or transformed issuer), in order to obtain admission to trading on a securities exchange, must provide the exchange with annual financial (accounting) statements in accordance with IFRS and/or US GAAP, in which was audited.

The liability for inaccuracies in documents providing access to the securities market is very high, therefore, it is necessary to approach the preparation of the company’s financial statements extremely carefully.

Due Diligence

It is also impossible not to note the issues of providing approved annual financial statements for conducting company audits (Due Diligence during the preparation of an IPO, M&A, acquisition of participation in a company or company assets), tax control measures by the tax authorities, desk audits by the securities market regulator, etc. .P.

At the preparatory stage of the IPO, financial audit reports of the company are compiled based on the audited annual financial statements for the last 3 years, which are then used to draw up the prospectus.

To draw up a report on the audit of a company for M&A purposes, the annual financial statements are also subject to verification, and the correctness and completion of all details and reporting indicators are assessed.

Approved annual financial statements - indicatorbest practice

For the most thorough preparation of reporting for approval by the general meeting, as well as assessment of the company’s performance for the past financial year, it is recommended to submit annual financial statements for preliminary review and approval by the board of directors, executive or supervisory body.

The charters of a number of large companies provide for the preliminary approval of annual financial statements by the board of directors, management board, and president.

The documents regulating the activities of a number of state-owned companies require mandatory audit of annual financial statements and consolidated financial statements, as well as their preliminary approval by the supervisory board.

Responsibility for failure to report

As already established above, in accordance with the legislation on accounting, annual financial statements submitted to state regulatory authorities are subject to mandatory approval by the highest management body of the company.

In practice, a situation often arises when the date of the annual general meeting is set later than the deadline for submitting annual financial statements. Many companies delay the submission of financial statements for this reason until they are approved by the general meeting. However, tax authorities and courts rightly believe that this circumstance is not a reason for failure to submit reports, and current legislation makes it possible to comply with the requirements of tax legislation and submit financial statements within the prescribed period.

Based on established judicial practice, even if the company’s charter provides for holding an annual general meeting after the deadline for filing annual financial statements, then in accordance with the requirements of the law the company needs to hold an extraordinary general meeting to approve the annual reports.

Article 126 of the Tax Code of the Russian Federation establishes liability for the taxpayer’s failure to submit within the prescribed period the documents provided for by the code and other acts of legislation on taxes and fees. This offense entails a fine from the company in the amount of 200 rubles for each document not submitted (Resolution of the Federal Antimonopoly Service of the Moscow District dated 08/04/2008 in case No. A40-59858/07-115-371, Resolution of the Federal Antimonopoly Service of the Central District dated 07/25/2007 on case No. A64-5050/06-15).

In addition, administrative liability is provided for failure to submit financial statements or refusal to submit them to state regulatory authorities. For such violations, a fine of 300 to 500 rubles is imposed on officials of the organization. (Article 15.6 of the Code of Administrative Offenses of the Russian Federation). Payment of a fine does not exempt the organization from submitting financial statements (Part 4, Article 4.1 of the Code of Administrative Offenses of the Russian Federation).

The Federal Law “On the Securities Market” establishes civil liability for losses caused to an investor and/or owner of securities as a result of the provision or disclosure of unreliable, incomplete and/or misleading information.

In addition, violation of legal requirements regarding the presentation and disclosure of information on the securities market is an administrative offense and entails quite severe liability for a legal entity and its manager.

So in accordance with Part 1 of Art. 15.19 of the Code of Administrative Offenses of the Russian Federation, failure to provide or violation by the issuer of the procedure and deadlines for providing information (notifications), as well as provision of information not in full, and/or unreliable information, and/or misleading information shall entail the imposition of an administrative fine on officials in the amount of 20,000 up to 30,000 rubles or disqualification for up to 1 year; for legal entities - from 500,000 to 700,000 rubles.

Part 2 of Art. 15.19 of the Code of Administrative Offenses of the Russian Federation provides for liability for non-disclosure or violation by the issuer of the procedure and terms for disclosure of information, as well as disclosure of information not in full, and/or unreliable information, and/or misleading information. This offense entails the imposition of an administrative fine on officials in the amount of 30,000 to 50,000 rubles or disqualification for a period of 1 to 2 years; for legal entities - from 700,000 to 1,000,000 rubles.

Based on judicial practice, the most common offense in this area - untimely disclosure of information, can be classified as a minor offense in accordance with Art. 2.9 of the Code of Administrative Offenses of the Russian Federation and the violator may be released from administrative liability. Insignificance occurs in the absence of a significant threat to protected social relations, while the absence of negative consequences or their elimination are not circumstances indicating the insignificance of the offense (clause 18 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated June 2, 2004 No. 10).

However, there is also the opposite judicial practice, based on which untimely disclosure of information is regarded as an encroachment on the order of public relations established by regulatory legal acts in the sphere of the securities market, and therefore it cannot be considered insignificant.

So, after analyzing the basic requirements for a company to have properly approved annual financial statements, we can conclude that compliance with the established requirements not only meets the interests of the company itself, but also makes the business more transparent, which increases the interest of potential investors and partners.

See sub. 11 clause 1 art. 48 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies” (hereinafter referred to as the Federal Law on Joint-Stock Companies), sub-clause. 6 paragraph 2 art. 33 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies” (hereinafter referred to as the Federal Law on Limited Liability Companies).

In accordance with Art. 13 of the Accounting Law.

See paragraph 2 of Art. 12 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting” (hereinafter referred to as the Law on Accounting).

See paragraph 3 tbsp. 88 Federal Law on joint stock companies and clause 3 of Art. 47 Federal Law on limited liability companies.

See paragraph 3 of Art. 52 Federal Law on joint stock companies and clause 3 of Art. 36 Federal Law on limited liability companies.

In accordance with clause 8.1.1. Regulations on disclosure of information by issuers of issue-grade securities, approved. By Order of the Federal Financial Markets Service of the Russian Federation dated October 10, 2006 No. 06-117/pz-n.

See clause 89 of Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n “On approval of the Regulations on accounting and financial reporting in the Russian Federation.”

According to the Civil Code of the Russian Federation and the Federal Law on Joint-Stock Companies, open joint-stock companies that have switched to a simplified taxation system are required to maintain, present and disclose financial statements.

Publication in newspapers and magazines accessible to users of financial statements, or distribution among them of brochures, booklets and other publications containing financial statements, as well as transferring them to territorial bodies of state statistics at the place of registration of the organization for provision to interested users.

acc. from clause 1.3 of the Order of the Ministry of Finance of the Russian Federation dated November 28, 1996 No. 101 “On the procedure for publishing financial statements by open joint-stock companies.”

See para. 3 p. 3 art. 88 Federal Law on joint stock companies.

According to paragraph 1 of Art. 30 of the Federal Law “On the Securities Market”, disclosure of information means ensuring its availability to all persons interested in it, regardless of the purpose of obtaining this information in accordance with a procedure that guarantees its finding and receipt.

According to paragraph 3 of Art. 30 of the Federal Law “On the Securities Market”, the provision of information means ensuring its availability to a certain circle of persons in accordance with a procedure that guarantees its location and receipt by this circle of persons.

See clause 8.3.7. Regulations on disclosure of information by issuers of issue-grade securities, approved. By Order of the Federal Financial Markets Service of the Russian Federation dated October 10, 2006 No. 06-117/pz-n.

International Financial Reporting Standards (IFRS; English International Financial Reporting Standards) - a set of documents (standards and interpretations) regulating the rules for preparing financial statements necessary for external users to make economic decisions regarding the enterprise.

Generally Accepted Accounting Principles (GAAP) are accounting standards used in the United States and some other countries. GAAP differs (in particular, from International Financial Reporting Standards) in that GAAP regulates in detail the procedure for accounting for certain practical situations.

See para. 2 p. 2 art. 15 of the Accounting Law and par. 3 clause 86 of the Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n “On approval of the Regulations on maintaining accounting and financial statements in the Russian Federation.”

See clause 2.4.5 of the Order of the Federal Financial Markets Service of the Russian Federation “On approval of standards for the issuance of securities and registration of securities prospectuses” dated January 25, 2007 No. 07-4/pz-n.

See clause 9 of Art. 22 of the Federal Law “On the Securities Market”; clause 8.1 ch. VIII. Appendix 8 to the Regulations on the disclosure of information by issuers of issue-grade securities, approved. By Order of the Federal Financial Markets Service of the Russian Federation dated October 10, 2006 No. 06-117/pz-n.

Listing is a set of procedures for including a security in one of the quotation lists of the stock exchange and monitoring the compliance of the securities and the issuer itself with the conditions and requirements established by the stock exchange.

See paragraphs. 14, 25 Appendix No. 40 to the Rules for Listing, Admission to Placement and Circulation of Securities on CJSC MICEX Stock Exchange.

See paragraphs. 5.1.1-5.1.2 Rules for admission of securities to trading at OJSC RTS Stock Exchange, approved. Board of Directors of OJSC RTS Stock Exchange (Minutes No. 09-21-3011 dated November 30, 2009) (hereinafter referred to as the RTS Admission Rules).

See paragraph 2 of Art. 31 Federal Law on limited liability companies; paragraph 3, clause 3, art. 33 Federal Law on joint stock companies; clause 2 art. 27.5-4 of the Federal Law “On the Securities Market”. Exceptions to this rule are indicated in paragraph 3 of Art. 27.5-4 of the Federal Law “On the Securities Market”.

See paragraph 1 of Art. 27.5.2 of the Federal Law “On the Securities Market”.

See clause 4.1.3 of the Rules, RTS Admission Rules.

See para. 2 p. 1 art. 18 Federal Law on limited liability companies.

Clause 3.5 of the Resolution of the Federal Commission for the Securities Market of the Russian Federation “On approval of the Regulations on additional requirements for the procedure for preparing, convening and holding a general meeting of shareholders” dated May 31, 2002 No. 17/ps.

Clause 5.5 of the RTS Admission Rules.

JSC Gazprom, JSC Aeroflot, JSC Russian Railways, JSC AVTOVAZ, JSC NK Rosneft, JSC Synergy.

See paragraph 1 of Art. 18 of the Federal Law “On the State Company “Russian Highways” and on Amendments to Certain Legislative Acts of the Russian Federation” dated July 17, 2009 No. 145-FZ; clause 1 art. 35 of the Federal Law “On the State Atomic Energy Corporation Rosatom” dated December 1, 2007 No. 317-FZ; clause 1 art. 9 of the Federal Law “On the State Corporation “Russian Technologies” dated November 23, 2007 No. 270-FZ; clause 1 art. 9 of the Federal Law “On the State Corporation for the Construction of Olympic Venues and the Development of the City of Sochi as a Mountain Climatic Resort” dated October 30, 2007 No. 238-FZ.

See Resolution of the Federal Antimonopoly Service of the North-Western District dated August 17, 2010 in case No. A56-72213/2009; Resolution 13 of the AAS dated April 19, 2010 in case No. A56-80327/2009; Resolution of the Federal Antimonopoly Service of the Volga District of March 5, 2010 in case No. A65-16385/2009.

See paragraph 11 of Art. 51 of the Federal Law “On the Securities Market”.

See Decision of the Moscow Arbitration Court dated 02/06/2007, 02/12/2007 in case No. A40-2623/07-17-24; Resolution of the Ninth Arbitration Court of Appeal dated December 19, 2006, December 26, 2006 No. 09AP-17166/2006-AK; Resolution of the Federal Antimonopoly Service of the Central District dated August 26, 2010 in case No. A54-120/2010.

In 1C:Enterprise solutions the report Financial statements is intended for the preparation of forms for both annual and interim financial statements of organizations starting from 2011 in accordance with the sample forms approved. by order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n (as amended by order of the Ministry of Finance of Russia dated April 6, 2015 No. 57n).

Report Simplified accounting statements form separate categories of organizations that have the right to use simplified methods of accounting, including simplified accounting (financial) reporting, and apply from reporting for 2012 in accordance with the sample forms of Appendix No. 5 to Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n “On Forms accounting statements of organizations" (as amended by the order of the Ministry of Finance of Russia dated April 6, 2015 No. 57n).

Annual accounting (financial) statements are prepared for the reporting year.

In some cases, interim accounting (financial) statements may be prepared for a reporting period less than the reporting year. To do this, in the start form of the report, if necessary, you can select a period - for a month, a quarter and a year on an accrual basis from the beginning of the reporting year.

Submission of reports in electronic form, starting with reports for 2015, is regulated by orders of the Federal Tax Service of Russia:

- dated December 31, 2015 No. AS-7-6/711@ - format for presenting accounting (financial) statements in electronic form”;

- dated December 31, 2015 No. AS-7-6/710@ - format for simplified accounting (financial) reporting in electronic form.

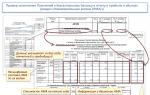

In accordance with the specified requirements for electronic presentation formats, the attribute “Date of approval of reporting” was added - see Fig. 1.

Rice. 1. Table 4.2 Presentation format

In 1C programs, you can indicate the date of approval of the annual financial statements on the Title Page Balance Sheet(Regulated reports on the menu 1C-Reporting) - see fig. 2.

Rice. 2. Indicator “Date of statement approval” on the title page of the Balance Sheet

In field Reporting approval date it is necessary to indicate the date of approval of the accounting (financial) statements.

The procedure for approving reporting is regulated by Part 9 of Article 13 of the Federal Law of December 6, 2011 No. 402-FZ and is carried out in the manner and cases established by federal laws. Approval of the company’s annual financial statements falls within the competence of the general meeting of shareholders (participants) (Article 48 of the Federal Law of December 26, 1995 No. 208-FZ “On Joint-Stock Companies”, Article 33 of the Federal Law of February 8, 1998 No. 14-FZ “On Companies” with limited liability").

The indicator is not required to be filled out.

note, if the indicator Reporting approval date is completed, the financial statements are not subject to corrections or adjustments.

Thus, in accordance with paragraph 10 of PBU 22/2010, in the event of correction of a significant error of the previous reporting year, identified after the approval of the financial statements, the annual financial statements approved by the owners are not subject to adjustment, replacement and re-presentation to all its users. This means that a significant error from last year is corrected in the current period in which it was discovered.

Read more about correcting errors in annual financial statements in

For several years now, accounting has been the responsibility of every legal entity, regardless of the taxation system it applies. Let us recall that until 2013, firms using the simplified tax system had the right to enjoy some kind of privilege and keep only tax records. Now there are no such concessions, so each company is required to submit a set of financial statements to the Federal Tax Service, as well as to Rosstat, by March 31 of the year following the reporting year. Of course, in addition to fulfilling this reporting obligation as part of accounting, the organization is not exempt from the need to provide reports and declarations to regulatory authorities based on the taxation system it applies, as well as its default status as an employer.

Composition of financial statements

If the organization is a small business, then it can prepare financial statements in a simplified form. In this case, the entire set will consist of only two forms: a balance sheet and a statement of financial results. All other companies submit financial statements in the following forms:

- balance;

- financial results report;

- statement of changes in capital;

- cash flow statement;

- explanatory note.

Deadline for submitting balance sheets and other forms for 2016

The deadline for submitting financial statements for both of these cases is the same: the last day for submitting reports for 2016 to the tax office and statistical agency is March 31, 2017.

But the timing for approval of reporting by the company’s owners in the accounting calendar for 2017 will be different. The founders of the LLC review and approve the balance sheet and other forms as part of the reporting in March-April of the year following the reporting one; for the shareholders of the JSC, a period from March to June is provided for the same purposes.

Deadlines for submitting tax reports for 2016

Tax reporting, unlike accounting, is not reviewed or approved by the owners of the organization. So, when planning dates for submitting reports, including for 2016, you need to focus only on the deadlines established for submitting reporting forms to the tax office and funds. As mentioned above, the specific types of declarations and calculations that a company is required to file depend on the taxation system it applies.

The most comprehensive set of both quarterly and annual reporting companies on OSN. Let us remind you that they are payers of income tax, VAT, transport tax and corporate property tax.

Annual declaration for income tax submitted at the end of the year by March 28. In addition, depending on the variation of tax calculation (quarterly or monthly), the company is also required to report to the tax authorities by the 28th day of the month following the reporting period. Moreover, the data in the declarations will be recorded on an accrual basis from the beginning of the year.

Reporting period for VAT is each separate quarter, so that the tax base for this payment is not transferred consistently from quarter to quarter. The deadline for submitting reports in this case is until the 25th day of the month following the end of the quarter.

Tax period according to corporate property tax is the calendar year. Reporting periods are the 1st quarter, half a year and 9 months of the year. Companies that have property on their balance sheets are required to submit quarterly reports no later than 30 calendar days from the end of the corresponding reporting period. The year-end declaration is submitted by March 30 of the year following the previous one.

And finally transport tax, a report for which is submitted only if the company owns a vehicle. The tax period in this case is the calendar year. Organizations submit their annual transport tax return no later than February 1 of the year following the expired tax period. In this case, quarterly reports are not provided.

Companies that have chosen as a base simplified taxation system, do not pay income tax and VAT and, accordingly, do not report on them. They are required to submit a “simplified” declaration at the end of the year. The deadline for this report is the same as for submitting the balance sheet: for 2016 - by March 31st. Firms submit property and transport tax declarations to the simplified tax system in the same manner as general tax regimes.

If any area of the company’s activity on the OSN or simplified tax system is transferred to the payment of imputed tax, then such a company is obliged, in addition to all of the above, to submit a quarterly UTII declaration. Its due date is the 20th day of the month following the reporting quarter.

Deadlines for submitting payroll reports

Each company, regardless of the fact of paying wages to its employees, is considered an employer and, therefore, is obliged to report accrued and paid contributions to the Pension Fund and the Social Insurance Fund.

Calculation by form 4-FSS RF submitted on an accrual basis at the end of the 1st quarter, half-year, 9 months and the year as a whole. The deadline for submitting it to the Social Insurance Fund is no later than the 20th day of the month following the reporting period. This deadline is established for submitting the form in paper form, that is, during a personal visit or when sent by mail. If you report electronically, then you must fulfill this obligation to the Social Insurance Fund no later than the 25th day of the month following the reporting period.

Form submission deadlines RSV-1 PFR also depend on the form in which it is submitted - printed, that is, paper or via electronic communication channels. In the first case, it must be provided before the 15th day, in the second - before the 20th day of the second month following the reporting quarter.

New for this year – monthly form SZV-M– a fairly simple report containing information about the TIN and SNILS number of employees. It must be submitted to the Pension Fund by the 10th day of the month following the reporting month.

Another “salary” tax – personal income tax, withheld from employees’ earnings and transferred to the budget by the employer, requires the submission of two reports at once: 2-NDFL at the end of the year by April 1, as well as quarterly 6-NDFL, which must be submitted to the Federal Tax Service by the end of the month at the end of the reporting quarter.

And finally, one more report, which can be conditionally classified as reports on employees - information on the average number of employees. It must be submitted once a year, no later than January 20th.

When filling the book. reporting for 2015 (OJSC), the field “Date of approval of reporting” has appeared in the Taxpayer Legal Entity. What date should be entered, since the reporting date has not yet been approved by the tax authorities?

If at the time of submission of the Balance Sheet the annual statements were approved by the owners, then indicate the date of approval. If not approved, do not fill it out.

Who, how and when is obliged to submit financial statements

Approval of annual reports

The annual financial statements must be approved (Part 9, Article 13 of the Law of December 6, 2011 No. 402-FZ). The decision on this is made by the general meeting of shareholders (participants)* (subparagraph 6, paragraph 2, article 33 of the Law of February 8, 1998 No. 14-FZ). Such a decision must be formalized in the minutes of the general meeting (clause 6 of Article 37 of the Law of February 8, 1998 No. 14-FZ).

There are no mandatory requirements for the minutes of the meeting of LLC participants in the legislation. But there are details that must be provided. This is the number and date of the minutes, place and date of the meeting, agenda items, signatures of the founders. The minutes of the general meeting of shareholders differ from the minutes of an LLC in that they are drawn up in duplicate and have mandatory details. These signs are listed in paragraph 2 of Article 63 of the Law of December 26, 1995 No. 208-FZ.

An example of how to draw up minutes of a general meeting of LLC participants. Approval of annual financial statements

The Charter of LLC "Trading Company "Hermes"" stipulates that annual financial statements are approved no later than March 20 of the following year. At the general meeting of participants, which took place on March 19, 2016, the financial statements were approved. The decision was made unanimously. The minutes of the general meeting of participants are compiled as follows.

Attention: The current legislation does not provide for liability for the fact that the annual financial statements are not approved*. But a fine is possible for failure to submit such reports to shareholders for approval.

Administrative liability in this case is established by Part 2 of Article 15.23.1 of the Code of the Russian Federation on Administrative Offences. This provision provides for punishment, in particular, for failure to provide or violation of the deadline for providing mandatory information (materials) in preparation for the general meeting of shareholders. Such materials also include the organization’s annual financial statements (Part 3 of Article 52 of the Law of December 26, 1995 No. 208-FZ).

The fine will be:

- for an organization – from 500,000 to 700,000 rubles;

- for officials – from 20,000 to 30,000 rubles. or disqualification for up to one year.

Situation: Is it possible to submit to the tax office annual financial statements that were not approved at the general meeting of participants (shareholders). The deadline for filing reports expires before the date for which the general meeting is scheduled.

Yes, you can.*

As a general rule, accounting (financial) statements are considered prepared after a paper copy is signed by the head of the organization (Part 8, Article 13 of Law No. 402-FZ of December 6, 2011).

But indeed, the period during which the annual financial statements must be submitted to the tax office does not coincide with the period during which they must be approved by the general meeting of the organization’s founders. Thus, the annual reporting of an LLC must be approved no earlier than two, but no later than four months after the end of the reporting year (