Property tax: new base and calculation in 1C. Property tax: new base and calculation in 1C Property tax 1C 8.3 is not filled out

In the program "1C: Accounting 8.0" (version 3.0), the system for working with taxes is modernized from time to time. For example, if previously in the program property tax declarations were only generated for sending to the tax authorities, now all types of declarations (for transport, land and property taxes) are generated and filled out automatically through regulatory operations. In this article we will take a closer look at this possibility using the example of property tax.

All the necessary components for setting up work with taxes are located in the “Directories” section. There we need the “Taxes” group, the “Property Tax” item

Property tax settings form includes 4 links

The item “Rates and benefits” indicates the property tax rate and the date from which it is valid for one or more organizations listed in the information base (Figure 3). You can also indicate all relevant tax benefits here.

If the organization’s accounting contains objects that have a special taxation procedure, then here you will find a form where you can enter all the necessary information about this object for its correct taxation.

Since tax accrual transactions can be generated automatically, you should clarify which value of the cost account to which the tax amount relates was set by the program by default, and check the necessary subaccounts accordingly. This setting is special in that it can be performed either in a single version (for all fixed assets and organizations), or separately for each organization and for some specific fixed assets.

The program has another useful setting. It is located in the “Payment Procedure” section (Figure 6). This form is used to indicate the due date for tax payment. In this case, you can choose whether advance payments are made or not, and if so, within what time frame. This regime can be established equally for all tax authorities, or differentiated for a specific tax authority.

When you check the checkbox for making advance payments, the regulatory operation “Calculation of property tax” is activated in the end months of the quarters - this is demonstrated in Figure 7. If the checkbox is not present, then this operation will be performed only in one and the last month of the year - December.

After all the “Month Closing” regulations have been generated, you can view the property tax accrual transactions by selecting the menu item for the operation of interest.

The procedure for calculating property tax for organizations is strictly regulated by Chapter. 30 of the Tax Code of the Russian Federation. This tax is set by each region independently. Its rate cannot be more than 2.2%.

For Russian companies, all real estate and movable property, which is a fixed asset, is recognized as objects on which taxes must be paid.

In accordance with the current legislation of our country, this type of tax is calculated using the following formula:

Tax amount = Tax rate * Tax base

During the tax period, the company has the right to make advance payments on property tax. As a result, the organization must make a payment at the end of the reporting period in an amount calculated using the following formula:

Tax amount = Tax rate * Tax base – Advance paid

The tax base is the average value of taxable property for the year. The specifics of its calculation are strictly regulated by the Tax Code of the Russian Federation.

For example, our organization has some property that is recognized as an object for taxation. We calculated its tax base, which amounted to 750 thousand rubles. In our region the rate is 2.2%.

During the year, the organization paid tax in advance in the amount of 12 thousand rubles. As a result, the total estimated tax will be:

750,000 rubles * 2.2% = 16,500 rubles

Taking into account previously paid advances, the amount of tax payable at the end of the billing period will decrease by 12,000 and amount to 4,500 rubles.

In the 1C 8.3 Accounting program, all property tax calculations are carried out automatically, including the preparation of a declaration. All you need to do is make the settings correctly.

Preliminary setup 1C

In the “Directory” section of the program there is an item in 1C “Property Tax”. This is where all the permanent data for tax calculation is entered.

As you can see in the image below, the settings are divided into four groups. Let's start our setup with the “Rates and Benefits” item.

This section reflects all changes in constants for calculating property tax, indicating the period of their validity. In our example, the program keeps records for several organizations at once, so each has its own line with settings.

In our case, for the organization Confetprom LLC, a property tax rate of 2.2% has been in effect since January 2016. No benefits apply. If you have any benefit, you must indicate its code, specifying the amount.

In the next section of the settings - “Payment Procedure”, we indicated to which tax authority Confetprom LLC is obliged to submit a declaration and pay tax. The default payment deadline is March 30.

If you plan to pay part of the tax amount in advance during the billing period, check the appropriate box and indicate the payment periods.

Among other things, we indicated in the settings that for all organizations and fixed assets, expenses will be reflected in account 26. This setting is made in the “Methods of reflecting expenses” section.

Tax return

Every year, before March 30 of the year following the reporting period, all companies are required to submit tax returns. In the 1C: Accounting program, they are generated in regulated reports, as shown in the image below.

All previously generated reports for all organizations for which records are kept in the program are stored here.

Click on the “Create” button and in the window that opens, go to the “All” tab if you have not added this declaration to your favorites. The property tax return is located in the “Tax reporting” folder.

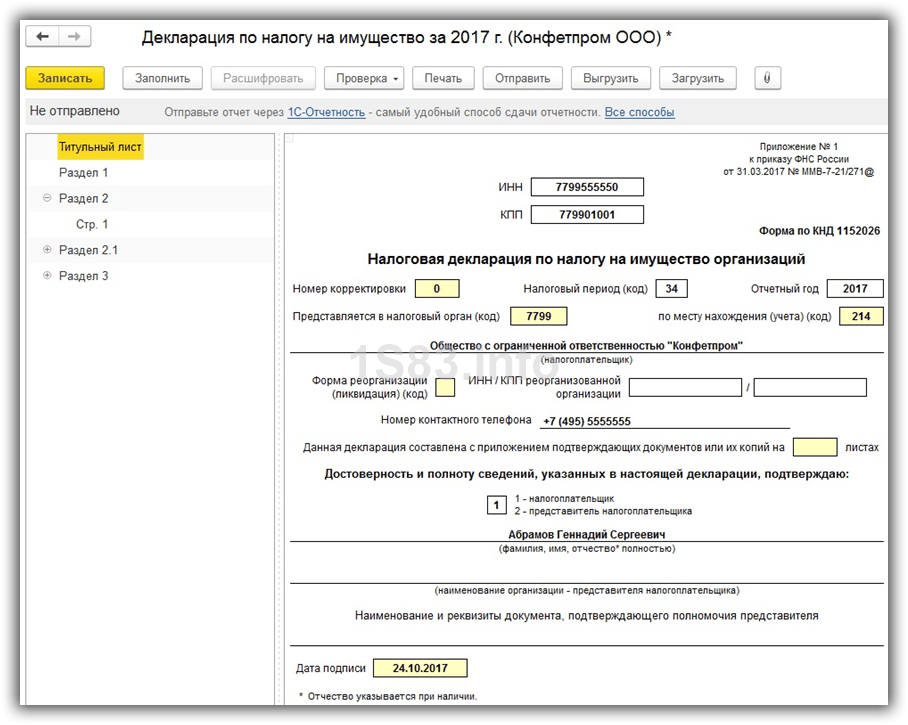

Before generating the declaration, the program will require you to indicate the organization and reporting period. In our case, this is a declaration for Confetprom LLC for 2017. Such a declaration must be submitted by March 30, 2018, as the program warns us about.

The declaration has three sections. The title page contains basic information about the tax authority and the company that submits it, indicating the reporting period.

Let's take a closer look at section 2. This is where our calculations were made. As can be seen in the figure below, the average annual value of the property of Confetprom LLC, which is subject to taxation, was 750,000 rubles. It consists of the value of the property in the context of each month.

Due to the fact that the tax rate in our region is 2.2%, the amount of tax that the program calculated was 16,500 rubles (750,000 rubles * 2.2%). The advance payment, if any, is also indicated here. During 2017, Confetprom LLC paid the tax inspectorate for property tax 12,000 rubles.

According to sections 2 and 3 (to be completed for real estate), section 1 is completed. In our case, Confetprom LLC does not own real estate, so the property tax payable will be only 4,500 rubles. This amount takes into account the previously paid advance.

note that tax reporting, like other regulated ones, may change periodically due to amendments to the current legislation. In this regard, it is recommended to follow updates and maintain the relevance of 1C: Accounting.

In this article I will tell you how to prepare a property tax return in the 1C program: Accounting for a government agency 8. ed. 1.0. Let me remind you that the procedure for taxing movable property has changed since January 1, 2015. As a general rule, the object of property taxation is movable and immovable property recorded on the balance sheet as fixed assets.

In this case, fixed assets belonging to the 1st or 2nd depreciation group are not recognized as an object of taxation. This rule applies regardless of the date of their registration as fixed assets.

At the same time, tax benefits apply to some items of movable property included in other depreciation groups.

Thus, movable property of organizations registered as fixed assets is exempt from taxation starting from January 1, 2013. The exception is for objects registered as a result of:

reorganization or liquidation of legal entities;

transfers, including acquisition of property

In this regard, movable property included in the 3-10 depreciation group and registered before 2013 is subject to property tax in the general manner.

So, the first thing you need to start preparing for drawing up a declaration in program 1C: Accounting of a government institution 8 is to check whether the property tax rates are indicated correctly in the fixed asset cards. To do this, go to the section “Fixed assets, intangible assets, legal acts” - “Fixed assets, intangible assets, legal acts”.

In the form that opens, select the tab “Tax accounting” - “Property tax”.

Open the entry by double-clicking on the line and check the information.

In the event that it is necessary to indicate property tax rates for a group of fixed assets, it is convenient to use the “Filling in property tax rates” processing, located in the menu “Assets, intangible assets, legal acts” - “Working with information registers for assets”.

For preferential property, a benefit code or a reduced tax rate is indicated. For those assets that are not recognized as objects of taxation, in the register of information “Property tax rates” should be set to “Not subject to taxation”.

All information about the established tax rates can be seen in the information register "Property tax rates", which can be found through the menu "Operations" - "Information register".

You can print a list of property through the menu "Actions" - "Print list".

Leave checkboxes for those columns that you would like to see in the list.

After this, you need to generate a report “Calculation of the average annual value of property”, located in the menu “Assets, intangible assets, legal acts” - “Reports on fixed assets, intangible assets, legal acts”.

The report divides property with a rate of 0 and a rate of 2.2.

In the 1C: BGU 8 program, regulated reports are intended for filling out tax calculations for advance payments for corporate property tax and a tax return for property tax: “Advances for property tax” and “Property, respectively.”

Quarterly it is necessary to submit a declaration “Advances on property tax”, and at the end of the year - “Property”.

The data for calculating the amount of the advance payment is contained in section 2. When filling out the report, the second page automatically becomes current, where the amounts of preferential property are indicated. Switch to the first sheet and check the data.

The amounts can be verified using the report “Calculation of the average annual value of property”, and you can also decipher the data from the report

When operating under the general taxation system, companies are required to pay many taxes, including the corporate property tax (hereinafter referred to as the tax). Timely, correct and complete calculation and payment of tax is guaranteed by accounting in the 1C system version 8.3. We will tell you below how to do this correctly and as efficiently as possible.

Tax base, rates

The object of taxation, as well as the rate, are established by Chapter 30 of the Tax Code of the Russian Federation. The maximum tax is 2.2%. At the level of constituent entities of the Russian Federation, the right has been granted to reduce the tax rate, as well as to provide additional tax benefits (Article 381 of the Tax Code of the Russian Federation provides for a list of federal tax beneficiaries). It is important to remember this when making settings in the 1C program, that is, before starting work, you need to check whether changes have been made in terms of tax regulation, both at the federal level and in regional legislation.

As a general rule, tax is calculated using the following formula: Tax = tax base (in rubles) * tax rate (in %) - the amount of advance payments (in rubles).

Calculation of property tax in 1C must begin with setting the necessary settings. You can configure the program in the menu “Main” - “Accounting Policy” - “Taxes and Reports Settings”.

Fig.1

On the left side, move the cursor over the line “Property Tax”.

Fig.2

Settings for editing open on the right, which reflect the requirements of current legislation, but the user can adapt some of them, focusing on personal benefits and tax rates in force in the region. So, let’s assume that in the region of business activity the current rate has been reduced to 1.9% since January 1, 2018.

If the organization has property that is subject to benefits, the code of the corresponding benefit must also be indicated in the “Benefits” section.

Also in this section it is possible to establish tax rates and establish benefits for individual fixed assets. To do this, click on the line “Objects with a special taxation procedure”.

Fig.3

In the window that opens, you can select a fixed asset object, set the date for applying the benefit, and also check a box confirming that this fixed asset object is not subject to taxation. In the “Registration” line (Fig. 4), there are three options to choose from:

- At the location of the organization;

- With a different OKTMO code (allows you to generate payment orders for tax payment using other details);

- In another tax authority.

Fig.4

In this tab, the accounting type code is also set. When you click on the active button, a window for selecting property groups opens by line.

Fig.5

In the “Tax benefit” line, you can choose to apply a reduced rate for the object, not apply benefits, or be exempt from taxation.

Fig.6

As an example, we will reflect the application of a reduced tax rate for the “Shop building” object in the amount of 1% (Fig. 7). The initial cost of the object is 12.0 million rubles (incl. VAT 18% - 2,160.0 thousand rubles).

Fig.7

Let's return to the "Taxes and Reports Settings" menu. When you click the line “Procedure for paying taxes locally” (Fig. 8), a menu opens that allows you to set settings for choosing a tax authority, the date of tax payment (by default - March 30) and making advance payments.

Fig.8

In the line “Methods of reflecting expenses”, the default method for reflecting expenses is set to account 26 “General business expenses”; you can change it if desired.

Fig.9

Tax return

The organization's property tax declaration (hereinafter referred to as the Declaration) at the end of the year is sent to the tax authority no later than March 30 of the next year, the so-called. The declaration for 2017 had to be submitted by March 30, 2018. This year, the corresponding “Tax calculations for advance payment...” (hereinafter referred to as the Calculation) for the 1st quarter, half a year and 9 months are submitted quarterly. The deadline for submitting Calculations is 30 days after the end of the relevant quarter.

Both documents (Declaration and Calculation) are regulated reporting documents, which can be found in the “Reports” - “Regulated Reports” section. Let's look at an example of creating a tax calculation based on the results of the 1st quarter of 2018 and calculate property tax for the specified period.

Fig.10

In the Declaration window that opens, the “Fill” button is active, with which the program will automatically fill out the Calculation. The calculation consists of a title page and three sections. The title page reflects information about the payer: TIN, KPP, name, reporting period, tax authority code, etc.

Fig.11

Section 1 “Amount of advance tax payment payable to the budget according to the tax authority” contains information on OKTMO, budget classification code, as well as the total amount of tax payable to the budget.

Fig.12

In our example, the organization acquired two fixed assets: “Shop building” worth 12 million rubles (incl. VAT 2,160.0 thousand rubles), the useful life of which is 240 months (20 years), and “Production line ice cream" worth 5.0 million rubles (including VAT 762.7 thousand rubles), the useful life of which is 75 months (6.5 years). In this case, the workshop building enjoys a preferential rate of 1%.

Fig.13

Line code (030) reflects the residual value of the workshop building as of 02/01/2018, equal to the acquisition cost minus VAT (12.0 million rubles - 2,160.0 thousand rubles) = 9,840.0 thousand rubles . On subsequent reporting dates, the residual value is reduced by the amount of monthly depreciation charges - 41.0 thousand rubles (9840.0 thousand rubles/240 months).

At the bottom of the first page of Section 1, the average cost for the reporting period, the reduced tax rate for a specific object and the amount of tax due to be paid to the budget for this object are indicated.

Fig.14

In this case, the average value of property consists of adding the value of property for each date of the period under review, divided by 4: (9048.0+9799.0+9758.0)/4=7349.3 thousand rubles.

Thus, we have determined the tax base, which must be multiplied by the tax rate (1%) = 7349.3*1% = 73,493 thousand rubles. At the same time, we need to remember that this is the annual tax amount, which must be divided into 4 periods (quarters) = 18,882 rubles (line 180).

The second page of Section 2 reflects the accrual of property tax on the second fixed asset object - “Ice cream production line” (Fig. 15), the upper part of this page also reflects the residual value of the equipment as of the reporting dates.

Fig.15

At the bottom of the described page you can see the tax rate established for this subject in the amount of 1.9%, as well as the total tax amount for this object in the amount of 14,894 rubles.

Fig.16

The total tax amount reflected in Section 1 (line 030) is the amount of tax on the two pages examined: 33,267 rubles = 18,373 rubles + 14,894 rubles.

Fig.17

Section 3 is formed in the case when an organization assesses tax on an object for which the tax base is determined by the cadastral value.

Thus, using the 1C program, calculating the tax required for payment is quite simple; just be careful about the initial data entered into the system.

The system for working with taxes in the 1C: Accounting 8.0 program (rev. 3.0) is constantly being improved. Previously, property tax returns could only be generated in the program and sent to the tax authorities. Now calculations, formation of transactions, and filling out declarations for property tax, transport and land taxes can be done automatically using routine operations. Read about how this works using the example of property tax in the article by 1C experts.

Everything you need to set up work with property taxes is located in the section Directories, in Group Taxes link Property tax(Fig. 1).

Rice. 1. Setting up property tax from the “Directories” section

In the property tax settings form that opens, there are four links (Fig. 2).

Rice. 2. Property tax setup form

Link Rates and benefits allows you to enter for a single or each of the organizations in the information base the actual property tax rate and the date from which it is valid (Fig. 3). In addition, here you can indicate all existing benefits for this tax.

Rice. 3. Enter the date from which the tax rate is effective

If there are objects registered in the organization to which a special taxation procedure applies, then using the link of the same name you can open a form for entering complete information about this object for correct taxation (Fig. 4).

Rice. 4. Entering information about objects with a special taxation object

Since the tax accrual posting is now generated automatically, it is necessary to specify or clarify the default value of the cost account to which the tax amount and, of course, the necessary subaccounts are assigned (Fig. 5). The peculiarity of the setup is that it can be performed not only in a single version (for all organizations and all fixed assets), but also separately for any organization and for any fixed assets.

Rice. 5. Setting up expense reflection

There is one more important setting that can be done using the link Payment procedure(Fig. 6). The proposed form indicates the tax payment deadline and asks you to choose whether advance payments are made, and if so (the box is checked), then within what time frame. This regime can be specified as the same for all tax authorities, or it can be established differentially for any one of them. Selecting the advance payment checkbox initiates the formation of a regulated operation Property tax calculation in the months of the end of the quarters, as can be seen in Fig. 7. If the checkbox is cleared, then such a routine operation is generated only in the last month of the year - December.

Rice. 6. Setting up the tax payment procedure

After the formation of all regulations Closing of the month, you can view the transactions for calculating property tax by selecting the appropriate menu item for the desired operation (Fig. 7 and Fig. 8).

Rice. 7. View transactions generated after the month close

Rice. 8. Document movements: Regular operation

To see or check how the amount of the accrued advance payment or the property tax itself is formed, you need to take advantage of the opportunity to create Help-calculation for this tax (Fig. 7 and Fig. 9).

See the video for more details.